An engineering guide to the modern rail mix

TL;DR. More changed in the plumbing of cross-border payments in the last eighteen months than in the previous decade. On 22 November 2025, SWIFT retired legacy MT payment messages and made ISO 20022 the only language for cross-border instructions. SEPA instant became mandatory across the euro area, screening and all. The first federal stablecoin frameworks went live on both sides of the Atlantic. For anyone building payment infrastructure, this means the interesting question is no longer which rail you pick — it’s whether your architecture treats a rail as a choice or as a rebuild. This is a field guide to the four rail families that matter in 2026, what actually changed on each, and the engineering decisions that follow.

The rail map moved under everyone’s feet

If you last drew your payments architecture in 2023, three things on that diagram are now wrong.

The messaging layer changed standard. The euro leg became instant-by-law. And a fourth rail family — regulated stablecoins — went from “interesting for treasury” to a live settlement option with actual rulebooks behind it. None of this showed up on a consumer banking app. All of it showed up in engineering backlogs.

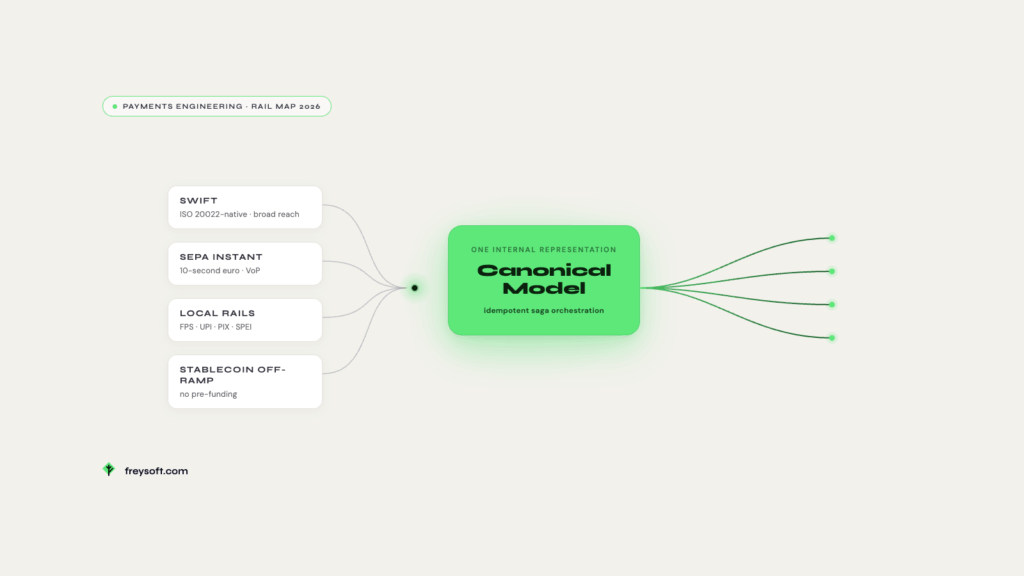

The temptation is to treat each of these as a discrete compliance project: a converter here, a screening upgrade there, a crypto experiment in a corner. That’s the expensive path. The cheaper path starts by seeing all four as the same shape of problem — a rail with its own protocol, its own data model, and its own regulator — feeding one internal representation of a payment. We’ll come back to that. First, the rails themselves.

SWIFT in 2026: correspondent banking, now ISO 20022-native

SWIFT is still the broadest-reach rail on the planet — roughly 11,500 institutions across 200-plus countries and territories — and it is still, fundamentally, a messaging network sitting on top of correspondent banking. What changed is the language.

On 22 November 2025, the MT/ISO 20022 coexistence period for cross-border payment instructions ended. The workhorse messages — MT103 (customer credit transfer) and MT202 (financial-institution transfer) — were formally retired in favour of their ISO 20022 equivalents (pacs.008, pacs.009) on the FINplus service, under the CBPR+ programme. There is no dual-format fallback for instructions anymore. By the cutover, around 80% of daily traffic was already ISO 20022, running at more than three million payment messages a day, so this was the end of a long migration rather than a big bang — but the runway is now gone.

The rest of the world’s high-value rails moved in lockstep. The euro clearing system (T2) migrated back in 2023; Fedwire completed its single-day ISO 20022 migration on 14 July 2025; Canada’s Lynx and Japan’s BOJ-NET aligned around the November window. And the standard’s demands keep tightening: fully structured postal addresses become mandatory across CBPR+ messages by the end of 2026, after which unstructured free-text addresses are rejected on payment instructions. A handful of categories (payment cancellations under the Stop-and-Recall process, some reporting messages) have a longer runway into November 2027, but the direction is one-way.

There’s a second SWIFT story worth putting on the roadmap. At Sibos 2025, SWIFT announced it will add a blockchain-based shared ledger to its stack — an EVM-compatible orchestration layer (built on Hyperledger Besu) intended to coordinate 24/7 cross-border settlement over tokenised deposits, and to interoperate, token-agnostically, with stablecoins and CBDCs. It progressed to an MVP in early 2026 with 40-plus institutions. It is not production infrastructure yet, and you should not plan a 2026 corridor around it — but it tells you where the messaging incumbent thinks value settlement is going, and it reuses ISO 20022, which is the thread tying this whole article together.

The engineering trap to avoid. The path of least resistance through the November deadline was to bolt an MX↔MT translation layer onto an MT-era core: you pass the compliance check, but you strip out most of the rich structured data ISO 20022 exists to carry, and you inherit a converter that needs perpetual upkeep and will start failing validations as the standard tightens. The durable move is to be ISO 20022-native — to model your internal transaction on the pacs schema so structured party data, purpose codes and structured addresses survive end-to-end. The structured-address mandate in particular is a real data-governance project: years of free-text beneficiary addresses have to be cleansed, validated and normalised before the 2026 deadline bites.

When SWIFT is the right rail: broad, high-value, or exotic corridors where no local instant rail exists; regulated correspondent flows where reach and auditability matter more than latency or per-transaction cost. SWIFT gpi gives you end-to-end tracking — but tracking is visibility, not speed.

When it’s the wrong rail: high-volume, low-value retail flows in any corridor where a local instant rail or an interlink already reaches the beneficiary. On cost and latency, SWIFT loses those every time.

SEPA and instant euro rails: the ten-second mandate

Inside the euro area, the SEPA question stopped being optional in 2025.

The Instant Payments Regulation (EU 2024/886), in force since April 2024, turned SEPA Instant Credit Transfer (SCT Inst) from a scheme banks could offer into one they must. Euro-area PSPs have had to receive instant euro transfers since 9 January 2025 and to send them — plus offer Verification of Payee — since 9 October 2025. The rulebook is strict: settlement within ten seconds, availability 24/7/365, the old €100,000 cap removed, and charges for instant transfers no higher than for standard ones. Non-euro-area EU member states follow on a 2027 timeline, with payment and e-money institutions due by 9 April 2027 and their VoP obligation by 9 July 2027.

Verification of Payee (VoP) is the part that quietly reshapes integration work. Before a transfer is authorised, the payee’s name and IBAN are checked against the receiving institution’s records, and the payer is told whether it’s a match, a partial match, or no match — for free, across all channels. It’s a fraud control, and it introduces a synchronous round-trip and a matching-algorithm problem (how do you handle “J. Smith” vs “John Smith”, trade names, virtual accounts?) into a flow that used to be fire-and-forget.

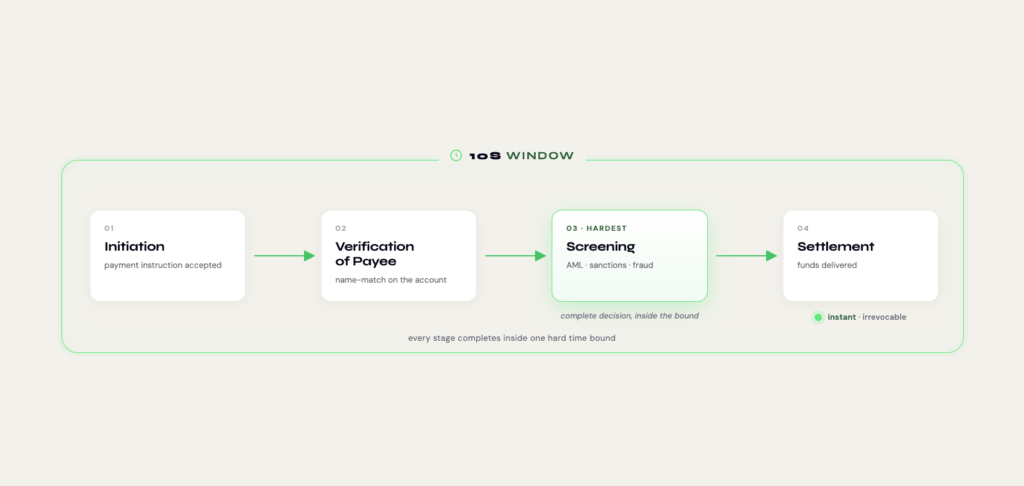

The engineering reality. Moving euro in ten seconds is the easy part; the rails (TIPS, RT1, STEP2) handle that. The hard part is running a complete AML, sanctions and fraud decision inside that ten-second window, around the clock, on a payment that is instant and irrevocable. Compliance stacks built for overnight batch review simply don’t fit the window — which is why real-time, threshold-calibrated screening (calibrated against your own transaction history, not left at vendor defaults) has become table stakes for anyone offering instant euro. Three other things follow from irrevocability: VoP has to be wired into the initiation flow (including the genuinely nasty case of bulk/file payments); liquidity has to be managed continuously because there are no weekend settlement windows to hide behind; and every step has to be idempotent — with instant, unrecallable money, a webhook that fires twice is a second payment you cannot claw back.

When SEPA instant is the right rail: any euro-denominated corridor, and increasingly cross-border euro reach as VoP and the European directory services mature.

When it’s the wrong rail: non-euro legs, obviously — and any flow where instant settlement buys you nothing and you’d genuinely prefer the liquidity control of a batch cycle.

Local rails: FPS, UPI, PIX, SPEI — and the interlinking wave

For the actual last mile into a country, the right rail is almost never SWIFT. It’s the domestic instant rail.

The UK has Faster Payments (FPS). India has UPI, now clearing north of 400 million transactions a day. Brazil has PIX, Mexico has SPEI, Thailand PromptPay, Singapore PayNow, Malaysia DuitNow, Indonesia BI-FAST and QRIS, the Philippines PESONet and FAST. Domestically these rails beat correspondent banking on every axis that matters to an operator: near-zero cost, settlement in seconds, and 24/7 availability. If you’re paying out into a market with a mature local rail, that rail is your endpoint.

What’s new in 2026 is that these rails are starting to interlink. Bilateral links have existed for a few years — PayNow–PromptPay since 2021, PayNow–UPI after it — but each one is bespoke: its own legal agreement, FX arrangement, compliance mapping and operational runbook. That doesn’t scale; connect n countries pairwise and you’re maintaining n² relationships. The response is a hub model. Project Nexus, incubated at the BIS Innovation Hub and now run by Nexus Global Payments (incorporated in Singapore in 2025 by the central banks of India, Malaysia, the Philippines, Singapore and Thailand), lets a domestic rail make one connection to reach every other rail in the network, using a common set of APIs and — again — ISO 20022 messages. First live cross-border transactions are expected around 2027, so this is a “design for it, don’t depend on it yet” item. But the trajectory is clear: the bespoke-per-corridor local integration is a shrinking asset.

The engineering reality. Every local rail has its own identity model and its own quirks: UPI’s virtual payment addresses, PIX’s alias keys, SPEI’s CLABE, FPS’s sort-code-plus-account. Each has its own limits, hours, reachability edge cases and error taxonomy. The only sane way to absorb that variety is a connector per rail that maps the rail’s protocol onto one internal representation of a transaction — so the rest of your system never learns what a CLABE is. Which, again, is the pattern underneath everything here.

When a local rail is the right rail: the last mile into any country with a mature domestic instant scheme — which by now is most of the ones that matter.

When it’s the wrong approach: committing to hand-build and forever maintain a bespoke point-to-point connection for every corridor. Interlinking will erode the value of that bespoke work; build so a local rail is a connector, not a special case.

Stablecoin off-ramps: settlement without pre-funding

The fourth rail family is the one that changed status most sharply — from crypto curiosity to a regulated settlement option with rulebooks.

Terminology first, because it’s where teams talk past each other. An on-ramp turns fiat into a stablecoin. An off-ramp turns a stablecoin back into local fiat in the destination country and credits it to a real account over a local rail. The off-ramp is the hard, regulated, valuable part.

Why an operator would care comes down to two structural advantages. Stablecoin value moves on public networks in seconds, bypassing the correspondent-banking chain entirely; and — this is the big one for emerging-market corridors — it eliminates pre-funding, the capital-intensive practice of parking money in a destination country before transfers can settle there. Move value on-chain, off-ramp it into local fiat at the far end, and the working capital that used to sit trapped in dozens of countries is freed. The scale is no longer trivial: the stablecoin market sat around $280–317 billion in early 2026, and on-chain stablecoin volume in 2025 exceeded $30 trillion — larger than a major card network’s annual throughput.

The reason this is a 2026 story and not a 2022 one is regulation. In the US, the GENIUS Act (signed July 2025) created the first federal framework for payment stablecoins, restricting issuance to permitted issuers with tightly constrained reserves; the OCC’s implementing rules were proposed in early 2026 with the full regime operational around January 2027, and the OCC granted conditional trust-bank charters to Circle, Paxos and others in December 2025. In the EU, MiCA has regulated e-money and asset-referenced tokens since June 2024, requiring significant issuers to hold a large share of reserves as deposits at EU credit institutions. One consequence matters directly for integration: the same brand of stablecoin is fragmenting by jurisdiction — a USDC minted and redeemable under EU rules is not operationally identical to one under US rules — so “we accept USDC” is no longer a single, global statement.

The engineering reality. An off-ramp is emphatically not “accept a stablecoin.” It is: jurisdiction-aware routing (which token, which issuer, which licensed liquidity partner in the destination); KYC/AML, Travel Rule and sanctions screening on both the crypto and the fiat legs; FX at the conversion boundary; a licensed local liquidity or virtual-asset partner to actually pay out; reconciliation across an on-chain ledger and a fiat ledger that fail in different ways; and clean handling of settlement finality and redemption. Orchestration layers are emerging to carry some of this — Circle’s Payments Network, Bridge, BVNK, Thunes’ stablecoin payouts across SWIFT-connected banks — but they don’t remove the compliance and reconciliation obligations, they relocate them. The right architectural stance is to treat the stablecoin network as one more connector against the same canonical model, with the same saga orchestration, the same idempotency guarantees, and the same threshold-calibrated compliance as every other rail.

When a stablecoin off-ramp is the right rail: emerging-market corridors where correspondent banking is slow and expensive and pre-funding is a real capital drag — and where you can secure a licensed off-ramp partner with clean redemption.

When it’s the wrong rail: regulated EU/US flows where a compliant instant fiat rail already does the job more cheaply and with far less regulatory ambiguity; and anywhere you cannot line up a licensed off-ramp and predictable settlement — in which case you’re taking on regulatory and liquidity risk the corridor doesn’t pay you for.

The pattern underneath: the rail is a connector, not an architecture

Look at the four families together and they collapse into one engineering truth.

ISO 20022-native SWIFT, SEPA Instant with VoP, a new local rail, a stablecoin off-ramp — each is a rail with its own protocol, data model and regulator. If your application code talks directly to each of them, then every rail is a rebuild, and you hit the wall the corridor-architecture work describes in detail: the choreography-to-orchestration rewrite that scale-ups typically face at corridor three or four. If instead each rail is a connector that maps onto a single canonical representation of a transaction — coordinated by deterministic, idempotent saga orchestration, with compliance thresholds calibrated to your own history — then absorbing the 2026 rail churn becomes connector work and configuration, not core-platform surgery.

This is where the difference between a generalist build and a specialist one stops being a slogan and becomes a line on a Gantt chart. A generalist team wires each new rail bespoke into the application and rebuilds when the count climbs. A team that has already built the canonical connector layer treats the ISO 20022 cutover, the VoP mandate, the interlinking wave and the first stablecoin off-ramp as new connectors against an interface that already exists. And the rail map is going to keep moving — SWIFT’s shared ledger maturing, Nexus going live around 2027, stablecoin rules finalising into 2027 — so the architecture worth having is precisely the one that makes the next rail a choice.

What this looks like in production

This isn’t a whiteboard argument. The published WorldRemit engagement is a working example of the canonical-model, multi-rail approach operating at scale — a platform spanning 130+ countries and 70+ currencies, handling 100,000+ transactions a day, delivered alongside a full Azure-to-AWS platform migration. Adding a corridor there is a connector problem, not a rewrite, which is the entire point.

The real-time-compliance-within-the-window problem is solvable too, not just assertable: in production screening deployments we’ve delivered sub-one-minute SEPA sanctions screening at a 0% error rate — evidence that you can run a complete compliance decision inside an instant rail’s constraints if the architecture is built for it rather than retrofitted.

Choosing your rail mix

The right rail mix is corridor-specific. SWIFT for broad reach and regulated high-value flows; SEPA Instant for euro; the local rail for the last mile into each country; a stablecoin off-ramp where pre-funding is killing your working capital and a licensed partner exists. That part you decide market by market.

The right architecture, though, is universal — and it’s the thing that determines whether next year’s rail change is a config edit or a quarter of engineering. If you’re mapping a 2026 rail roadmap and you’re not sure which of those two your current stack gives you, that’s exactly the question a short scoping conversation is built to answer.